I spent my first eight months as a digital nomad dangerously confused about insurance. I had a World Nomads travel insurance policy and assumed I was completely covered for any medical situation. Then I tried to get a routine checkup in Lisbon for a persistent cough that wouldn’t go away. The clinic visit cost €85. When I submitted my claim, World Nomads rejected it immediately. “Travel insurance covers emergencies only,” the email explained. “Routine medical care is excluded from your policy.”

That rejection forced me to understand something most new nomads miss: travel insurance and health insurance are fundamentally different products designed for completely different situations. Using the wrong one leaves you exposed to massive financial risk or paying unnecessarily for coverage you don’t need.

This confusion costs digital nomads thousands of dollars annually through denied claims, duplicate coverage, or gaps that only become apparent during medical emergencies. After three years of navigating international insurance and speaking with dozens of nomads about their coverage mistakes, I’ve learned exactly what distinguishes these two insurance types and which one actually makes sense for location-independent professionals.

the fundamental difference between travel and health insurance

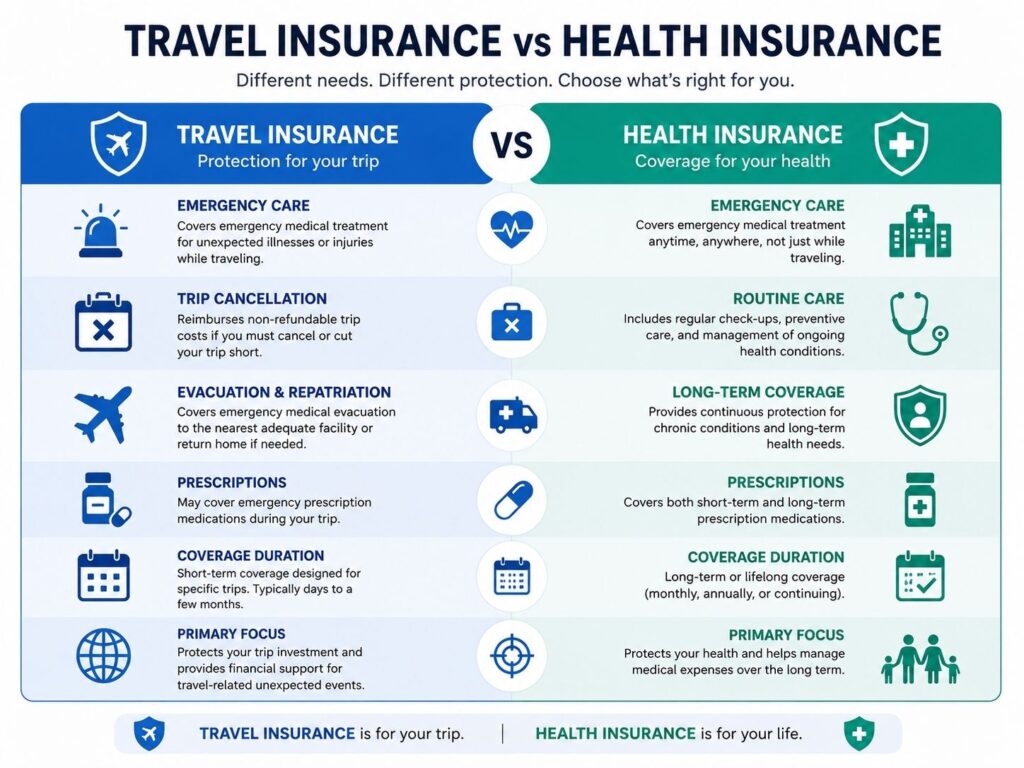

Travel insurance is designed for temporary trips with defined start and end dates. You’re leaving home for two weeks in Thailand or three months backpacking Europe, then returning to your permanent residence where you maintain regular health insurance. Travel policies protect against trip-specific risks: flight cancellations, lost luggage, emergency medical situations while away from home, and medical evacuation back to your home country.

Health insurance provides ongoing medical coverage for people living somewhere long-term. It covers routine doctor visits, prescription medications, preventive care, specialist consultations, chronic condition management, and hospitalization. Health insurance assumes you’re a resident of the coverage area who will access healthcare regularly over months or years.

The critical distinction is intent and duration. Travel insurance treats medical care as an unexpected emergency interrupting your trip. Health insurance treats medical care as a normal part of life requiring consistent access to healthcare providers.

Digital nomads fall into a gray area between these categories. We’re not taking temporary trips from a permanent home. We’re living abroad semi-permanently, moving between countries every few months or years. We need emergency protection like travelers but also need reliable access to healthcare like residents.

This unique situation is why specialized digital nomad insurance emerged as a category combining elements of both travel and health insurance while fitting neither traditional definition perfectly.

what travel insurance actually covers

Travel insurance focuses on protecting your trip investment and covering medical emergencies that occur while traveling. Understanding exactly what’s included prevents the surprise I experienced with my rejected routine care claim.

Emergency medical treatment represents the core coverage. If you’re in an accident, develop sudden illness, or face any acute medical situation requiring immediate treatment, travel insurance covers emergency room visits, hospitalization, surgery, and related care up to your policy limit (typically $50,000 to $500,000).

Medical evacuation covers transportation to adequate medical facilities if local care is insufficient. If you’re seriously injured on a remote island in Indonesia, travel insurance pays for emergency airlift to a hospital capable of treating your condition, potentially costing $50,000-100,000 that would otherwise come from your pocket.

Trip cancellation and interruption reimburses non-refundable expenses if you must cancel or cut short your trip due to covered reasons like illness, injury, or family emergencies. This matters more for traditional tourists than digital nomads since our “trips” are essentially continuous.

Lost or stolen baggage provides reimbursement for belongings lost by airlines or stolen during your trip. Coverage limits are typically low ($500-1,500), so it won’t replace your laptop and camera, but it helps with clothes and basic items.

Adventure activity coverage is where travel insurance sometimes exceeds health insurance. Policies from World Nomads and similar providers cover injuries from activities like scuba diving, rock climbing, or motorcycling that traditional health insurance often excludes.

The key limitation is that travel insurance only covers unexpected emergencies. Routine care, prescription refills for ongoing medications, preventive checkups, dental cleanings, mental health counseling, and treatment for pre-existing conditions are almost universally excluded.

what travel insurance does not cover

Understanding exclusions is just as important as understanding coverage. These gaps catch nomads by surprise:

Pre-existing medical conditions are excluded or severely limited on virtually all travel insurance. If you have diabetes, asthma, high blood pressure, or any ongoing health condition, travel insurance won’t cover related care. Some policies offer pre-existing condition waivers if you purchase coverage within 14-21 days of booking your trip and meet other criteria, but these waivers rarely apply to digital nomads who aren’t booking traditional vacation packages.

Routine and preventive care receives no coverage. Annual physical exams, vaccinations, health screenings, prescription refills for maintenance medications, dental cleanings, eye exams—all excluded. You pay entirely out-of-pocket for routine healthcare even with travel insurance.

Mental health services are typically excluded or severely limited. If you need therapy, psychiatric care, or treatment for anxiety or depression, most travel insurance provides little or no coverage.

Pregnancy and maternity care is almost always excluded from travel insurance. Some policies cover unexpected pregnancy complications if they arise during travel, but routine prenatal care, delivery, and newborn care receive no coverage.

Extended treatment presents complications. Travel insurance covers emergency treatment to stabilize your condition, but if you need ongoing care over weeks or months, coverage becomes murky. Policies may stop paying after initial emergency treatment even if full recovery requires extended care.

Home country limitations surprise many nomads. Most travel insurance policies either exclude your home country entirely or limit home country coverage to very short visits (30 days maximum). SafetyWing allows 30 days of home country coverage per 90-day period, but if you spend more time home, you’re uninsured.

what international health insurance covers

International health insurance operates like domestic health insurance but provides coverage across multiple countries. It’s designed for expatriates, international workers, and long-term travelers who need ongoing healthcare access rather than just emergency protection.

Comprehensive medical care forms the foundation. Inpatient hospitalization, outpatient doctor visits, specialist consultations, diagnostic tests, surgery, and emergency care all receive coverage. You can visit doctors for any medical need, not just emergencies.

Prescription medications are covered under most international health plans, either through pharmacy benefits or as part of outpatient care. If you take daily medications for chronic conditions, this coverage saves hundreds or thousands monthly.

Preventive and routine care distinguishes health insurance from travel insurance. Annual checkups, cancer screenings, vaccinations, and other preventive services receive coverage on comprehensive plans. Some basic plans exclude preventive care to reduce premiums, so check your specific policy.

Pre-existing conditions receive coverage on many international health insurance plans after waiting periods, typically 12-24 months. This means if you have an ongoing condition requiring regular care, international health insurance eventually covers it, unlike travel insurance which permanently excludes pre-existing conditions.

Maternity coverage is available as an add-on or inclusion on comprehensive plans. Prenatal care, delivery, and newborn care all receive coverage, though waiting periods (typically 10-12 months) apply to prevent people from purchasing coverage only after becoming pregnant.

Mental health services receive better coverage on international health insurance, with many plans covering therapy, psychiatric care, and mental health medications. Coverage limits vary, with some plans capping mental health benefits at $5,000-10,000 annually.

Dental and vision care can be included as add-ons on comprehensive international health insurance. Basic emergency dental receives coverage on most plans, while routine cleanings and major dental work require specific dental coverage riders.

The tradeoff for this comprehensive coverage is cost. International health insurance typically costs $200-800 monthly depending on age and coverage level, compared to $45-120 monthly for travel insurance. You’re paying for ongoing healthcare access rather than emergency-only protection.

how digital nomad insurance bridges the gap

Recognizing that traditional travel insurance doesn’t meet nomad needs but comprehensive health insurance is prohibitively expensive for many location-independent workers, specialized digital nomad insurance emerged as a hybrid category.

SafetyWing’s Nomad Insurance exemplifies this approach. It operates as travel medical insurance covering emergency care, hospitalization, medical evacuation, and some outpatient treatment for acute illness or injury. The monthly subscription model ($56 for under-40 travelers) with automatic renewal fits nomadic lifestyles better than traditional travel insurance with fixed trip dates.

The coverage is more flexible than standard travel insurance, allowing continuous renewal for months or years rather than limiting coverage to 90-180 days like most travel policies. You can purchase coverage while already traveling and activate it immediately, unlike traditional travel insurance requiring purchase before departure.

Limited home country coverage (30 days per 90-day period with SafetyWing) lets you visit home occasionally without losing coverage completely. Traditional travel insurance typically excludes your home country entirely.

However, digital nomad insurance maintains travel insurance limitations. Pre-existing conditions remain excluded, routine care receives no coverage, and the focus stays on emergency medical situations rather than comprehensive healthcare access.

This hybrid model works well for young, healthy nomads who rarely need medical care and primarily want protection against catastrophic expenses. It falls short for nomads with chronic conditions, those planning families, or anyone wanting routine healthcare access without paying entirely out-of-pocket.

which type of insurance makes sense for different nomad profiles

Your ideal insurance depends entirely on your personal situation, health status, age, and financial resources.

Young healthy nomads (20s-30s, no chronic conditions): Travel insurance or digital nomad insurance makes the most sense. You probably won’t need routine care frequently, and paying $50-80 monthly for emergency protection provides excellent value. SafetyWing or Genki offer affordable coverage meeting your needs without overpaying for comprehensive benefits you won’t use.

Mid-career nomads (30s-40s, generally healthy): Digital nomad insurance still works well, though consider your changing health needs. If you’re starting to need occasional doctor visits for minor issues, budget for out-of-pocket healthcare expenses in addition to insurance premiums. Countries like Portugal, Mexico, and Thailand offer affordable private healthcare that costs less than upgrading to comprehensive insurance.

Nomads with chronic conditions: International health insurance becomes necessary despite higher costs. Paying $300-500 monthly for comprehensive coverage that includes your ongoing condition is cheaper than paying thousands out-of-pocket for specialist visits, prescription medications, and regular monitoring. Cigna Global, Allianz Care, or Aetna International provide coverage for pre-existing conditions after waiting periods.

Families with children: Comprehensive international health insurance is essential. Children need regular pediatric checkups, vaccinations, and occasional sick visits. Maternity coverage becomes critical if you might expand your family. The $500-800 monthly cost for family coverage is substantial but necessary for responsible parenting while traveling.

Older nomads (50+): Consider comprehensive international health insurance even if you’re currently healthy. As you age, the likelihood of needing regular medical care increases. Emergency-only coverage leaves you paying entirely out-of-pocket for increasingly frequent healthcare needs. The peace of mind from comprehensive coverage justifies the premium.

Adventure-focused nomads: Travel insurance from providers like World Nomads offers better adventure activity coverage than most health insurance. If you regularly scuba dive, rock climb, or participate in extreme sports, paying slightly more for travel insurance with adventure riders protects you during risky activities.

the hybrid approach many experienced nomads use

After years of navigating this challenge, many experienced nomads adopt a hybrid strategy combining multiple insurance types for comprehensive yet affordable coverage.

The most common approach uses travel or digital nomad insurance for emergency coverage while paying out-of-pocket for routine care in countries with affordable healthcare. You maintain SafetyWing at $56 monthly for catastrophic protection, then pay $30-80 for doctor visits in Portugal, $25-50 in Mexico, or $40-100 in Thailand when you need routine care.

This works brilliantly in countries where private healthcare costs less than insurance premiums. An annual checkup in Thailand costs $60-100. Why pay an extra $200 monthly for health insurance that covers that checkup when you can simply pay cash?

Some nomads maintain basic travel insurance for emergencies plus local health insurance in their primary country of residence. If you spend six months annually in Portugal, purchasing Portuguese health insurance at €100-150 monthly covers your healthcare during that period, while travel insurance protects you during the other six months exploring other countries.

Others maintain travel insurance most of the year but upgrade to comprehensive international health insurance during predictable high-healthcare periods. If you’re planning pregnancy, need surgery, or expect significant medical needs, upgrade temporarily to comprehensive coverage, then downgrade back to travel insurance once those needs pass.

The key is actively managing your insurance rather than assuming one policy type works for all situations across years of nomadic life.

cost comparison over one year

Understanding the true cost difference between insurance types requires looking beyond monthly premiums to include out-of-pocket healthcare expenses.

Travel insurance scenario (35-year-old with SafetyWing):

- Monthly premium: $56

- Annual premium: $672

- Routine doctor visit in Mexico: $45

- Prescription for sinus infection: $15

- Annual checkup in Thailand: $85

- Dental cleaning in Portugal: $65

- Total annual cost: $882

International health insurance scenario (35-year-old with basic Cigna plan):

- Monthly premium: $280

- Annual premium: $3,360

- Co-pays for same care: $100

- Total annual cost: $3,460

For a healthy nomad requiring minimal medical care, travel insurance saves $2,578 annually. That’s significant money for nomads operating on modest budgets.

Travel insurance with chronic condition:

- Monthly premium: $56

- Annual premium: $672

- Quarterly specialist visits (4 at $120): $480

- Monthly medication ($80 × 12): $960

- Annual lab work: $200

- Total annual cost: $2,312

International health insurance with chronic condition:

- Monthly premium: $350 (higher tier with pre-existing coverage)

- Annual premium: $4,200

- Co-pays and deductible: $500

- Total annual cost: $4,700

Even with a chronic condition, travel insurance plus out-of-pocket care costs $2,388 less annually. However, this assumes stable condition requiring only routine monitoring. One hospitalization or serious complication quickly reverses this calculation, potentially costing $20,000-50,000 out-of-pocket with travel insurance versus $2,500-5,000 maximum out-of-pocket with comprehensive health insurance.

making your decision

Choosing between travel insurance and health insurance requires honest assessment of your health status, risk tolerance, and financial situation.

If you’re young, healthy, have emergency savings covering $5,000-10,000 in potential medical costs, and rarely need medical care, travel insurance or digital nomad insurance provides sufficient protection at affordable prices.

If you have chronic conditions, take regular medications, anticipate needing ongoing medical care, or want peace of mind from comprehensive coverage, international health insurance is worth the premium despite higher costs.

If you’re somewhere in between, consider the hybrid approach of maintaining emergency travel insurance while budgeting for out-of-pocket routine care in affordable healthcare countries.

Remember that insurance represents protection against worst-case scenarios, not necessarily the most cost-effective way to pay for healthcare you know you’ll need. A healthy nomad paying $3,500 annually for comprehensive insurance they never use is overpaying. But a nomad with basic travel insurance facing $50,000 in hospitalization costs discovers too late that saving $200 monthly on premiums was a catastrophic mistake.

The right choice balances adequate protection against your actual risks with costs that fit your budget without sacrificing other aspects of the nomadic lifestyle you’ve worked hard to achieve.

As you evaluate options, understanding the common mistakes nomads make when choosing and using their insurance helps you avoid expensive errors. Learn from others’ experiences by exploring the seven critical digital nomad insurance mistakes that could cost you thousands including coverage gaps, overlooked exclusions, and claim denial situations that leave even insured nomads paying massive bills out-of-pocket.